#2 Avoiding Debt Avalanches 💳

The ripple effect of minimum payments (The Black Friday edition)

Hello, and welcome to the next edition of Tenets of Stoic Wealth. 😊

The aim of this newsletter is to build on some of the ideas relating to personal finance that I talk about in the visuals that I share on Twitter, LinkedIn and Instagram, while allowing space to get into more detail about how you can apply it to your own life.

This is not financial advice. It’s simply somewhere to learn about personal finance in a different and (hopefully 🤞🏼) more interesting way.

After all, it’s far too important a topic to leave to chance!

Let’s dive in!

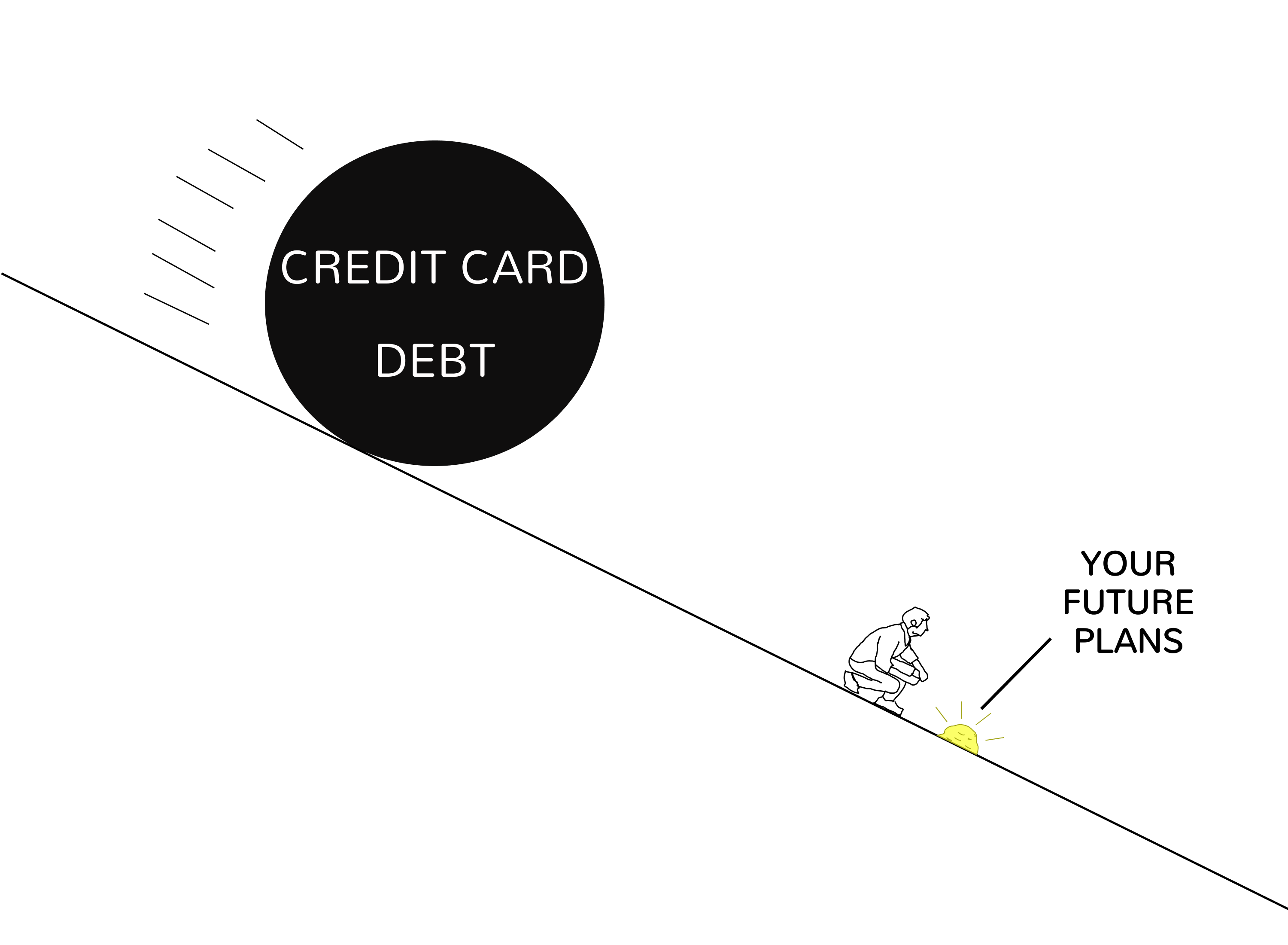

What’s Wrong with Debt?

Debt is the term used to describe money that you owe. That can be money that you owe the bank in the case of a mortgage, or a loan from the dealership for your car or the credit card company, to name but a few examples.

Now, it is worth remembering that debt in itself is not necessarily bad.

Used correctly, debt can be a powerful tool that works in your favour, and we’ll be sure to look at that in a separate edition.

However, in the case of credit card and other high interest debt, the problem is not so much the debt itself, but the interest that builds on top of it.

The Problem with Credit Cards

When you spend money on a credit card, it’s not your money. The credit card company pays for your new clothes, shoes and holidays. As the money doesn’t come out of your bank account, it’s easy to get carried away, spending money you don’t have while your credit card balance quietly accumulates in the background.

At the end of the month, they’ll send you a statement. Suddenly, you realise how fast those shopping sprees, nights out and unnecessary purchases add up. Unable or unwilling to pay off the balance in full, you pay some of it off and you’ll “get round to paying the rest off later” you think. This is the most dangerous mistake that you can make.

You forget about it and keep using the card, only to receive the double shock a month later of the combined bill of everything you spent that month plus what was left over. Only now they’ve added interest to what you owed from the last month, and it’s a lot more…

The longer you leave paying of the card by making minimum payments, the more interest will accumulate and the more expensive it is for you.

How do I avoid this?

Only ever spend what you can afford to pay back.

The moment you don’t pay back the credit card in full, they start charging you interest, and that’s when it starts to get out of hand.

Set a lower limit on your card.

This means that you never end up with an enormous bill you can’t afford. Setting the limit to something that you could easily pay if you max out your credit card means you’ll never be at the mercy of sky-high interest rates.

Automate your credit card balance payments.

Set your current account to pay off the credit card, each month, in full. As we saw in the last edition, building sustainable wealth depends largely on the systems that you put in place. (It may sound obvious, but one of the best ways to build wealth is to avoid getting into high interest debt!)

So, be careful spending money that isn’t yours.

Have systems in place to do things for you, and you’ll never have to worry about getting crushed under an avalanche of debt.

Because sooner or later, the bill will come due, and it will only get more painful if you’re unable to pay it first time round.

And that’s it for this edition of Tenets of Stoic Wealth.

I hope that you enjoyed it, and please feel free to share with any friends, family, third cousins and pets who may find it useful! You can do that here:

If you have any thoughts or feedback, I’d love to hear from you! You can either reply to me here or reach me at my email hello@stoicwealth.co.uk

See you all in the next one!

Felix