#18 Hedonic Adaptation 🔄

#18 Hedonic Adaptation 🔄

How to get off the treadmill to nowhere and move forward, fast!

Another weekend begins, heralded by the arrival of the latest edition of Tenets of Stoic Wealth arriving right to your inbox!

We’ve already established that inflation is one of the silent killers of wealth, but there is actually another, much more potent and infinitely more difficult enemy to fight: hedonic adaptation.

In this edition we’ll take a look at what it is, how it can set back your retirement and financial freedom by YEARS and what you can do about it.

The best bit? You’re completely in charge of the outcome.

Lace up your boxing gloves, because we’re about to get stuck in!

What is Hedonic Adaptation?

We live in a period of such abundance in which the only limit on our ability to enjoy ourselves and purchase whatever we want is the amount of money in our bank accounts and the cheap credit we can apply for.

We suffer through our jobs in order to receive a paycheck at the end of the month, allowing us to go out and spend it on whatever we want in order to give ourselves a sense of meaning and justify the hours spent behind a desk.

And as we get older, and we climb the career ladder, our income tends to increase. Our friends, direct and powerful influences on our own behaviour, also move up to higher salaries, and the things we permit ourselves to spend money on increase in value correspondingly.

A date night might have been a pizza at home with your favourite series on Netflix, but now you take a taxi to a posh restaurant, posting the pictures online as you go. There wasn’t really anything wrong with your old car, but your new fancy one is so much more fitting for someone of your stature and earning, right?

Along with the eye watering monthly payments that go with it, you lose your ability to enjoy the more low-key things that once brought you happiness. Yet despite all the upgrading, you don’t really find yourself any happier.

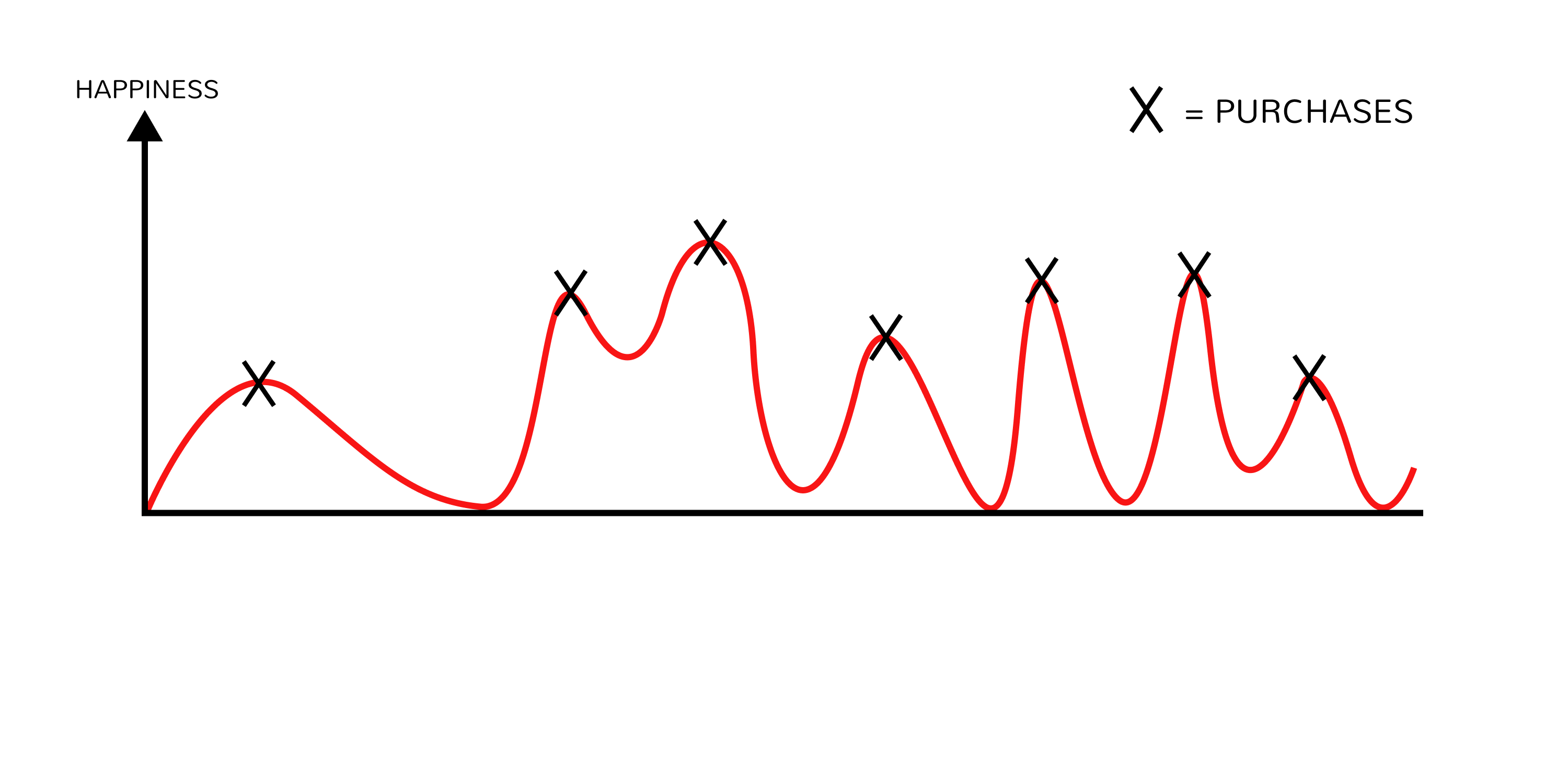

This, in a nutshell, is hedonic adaptation.

As our means and wealth increase, we spend more and more on “levelling up” our possessions, experiences and life. We tell ourselves that the newer car, the more expensive clothes, the new living room suite will make us happier.

And the kicker is that they do.

But only for a very limited time, because after the ‘newness’ wears off, you become accustomed to the new situation and your base happiness goes back to the same as it was before.

You should absolutely enjoy spending money on the things that are important to you, but consciously, rather than including them as part of a rapidly ballooning monthly list of expenses that your mentality from 10 years ago would have laughed at the ridiculousness of.

The Hidden Danger

The danger here is the effect that this has on your ability to reach financial freedom, and that it can set you back by years.

Rather than any one sudden event, it is the slow creep of ‘lifestyle inflation’.

You work hard to reach a certain level, or a particular income, and all of a sudden that restaurant you loved going to starts to look a bit basic. The car that was fine for taking you to work and going on holiday suddenly looks old and embarrassing. Do you really want to be seen driving around in that?

And so we upgrade our lives, our possessions, to more fit in with the level that we consider ourselves to be at.

And although we almost certainly earn more than we did, we’re not saving a greater percentage of our income, and we’re probably not all that much happier than we were either.

Because we chase the happiness that we think will be provided by material possessions, we spend money on those, rather than building our freedom fund that will set us free from working for money. And even though we get a short term rush, our happiness always reverts back to a baseline.

But just as we adapt to spending more, we can adapt to spending less.

And when we do that, we free up more money to invest for our future, allowing us to reach financial freedom faster. I’m not necessarily talking about retirement, but getting to a point where money no longer dictates what you choose to work on and dedicate your time to.

And that will certainly have a long term impact on your happiness.

What To Do About It

The science is pretty clear on what provides human beings with happiness, which in no particular order include meaningful work, relationships, community, health and freedom.

None of those things are on sale in the shopping centre.

Instead they have to be worked for and developed over time, and something that will absolutely help you get there is a level of financial freedom that will be harder to achieve if you are stuck on the addictive cycle of endlessly increasing consumption.

It’s not your fault either. We’re constantly bombarded by adverts telling us to buy this, buy that, look at how happy these people are with this fancy new thing. Advertising that plays on our emotions is a powerful weapon that is used at will to transfer our hard earned money from our wallets and investments to corporations’ bank accounts in return for the promise of happiness.

Look around you for a moment.

How many things in your home are sitting in drawers, cupboards, bought, used and now forgotten (some of them still in plastic, not even touched!)

The cravings are real, and the item will increase your happiness, but only initially.

So if we climb off the hedonic treadmill that everyone else is on, and we realise that we were able to live happily when we were earning 50% less, then surely that extra money we earn now can be put to a better use?

The maths agrees.

If you save 10% of your income, in 9 years you will have saved enough for 1 year of living expenses.

But if you can increase your savings rate to 25%, it will take you just 3 years to afford 1 year of living expenses.

This is obviously net of inflation and investment returns, but the numbers are clear.

You just cut your time to financial freedom by TWO THIRDS!

And if you can get it to 50%, then every year worked covers an additional year of expenses. Considering that financial freedom is roughly having 25 times your annual expenses invested, your obligatory working life starts to shrink dramatically.

Your lifestyle inflation and creeping expenses affect your ability to save and invest because you’re busy spending it on things that aren’t important. You want to skip straight to dessert, but in taking the short cut to what will bring you real happiness, you end up with just the crumbs left on the plate.

Hedonic adaptation significantly affects your savings rate, and therefore, your time horizon to reaching financial independence.

Just like zooming out to look at the bigger picture with investing, we can do the same here.

Is it worth sacrificing our hard earned money for some short term addictive pleasure?

Or using it towards a much greater goal that will allow us to live more fulfilling lives from a place of security and abundance, and leave us not with a last gasp retirement on the little that we have been able to scrimp and save in between purchases, but multiple decades of living life to the fullest, free from the burdens carried by those trapped on the hedonic treadmill.

The choice is yours.

Choose wisely.

F.