#10 The 5 Step Process to Building Wealth 👣

Breaking it down into actionable steps to get you started right away.

Here at Tenets of Stoic Wealth, we’re all about helping you to build sustainable wealth. Sustainable in the sense that you can meet all your financial needs, be self sufficient, and be free to enjoy life without money issues getting in the way.

We’ve already looked at a great number of the key stages of building wealth, and I’ll be attaching links to previous editions where I go into more detail on each subject. It can be easy to think that it is an overly complex subject, something far out of reach, unattainable.

To counter that, I have decided that we’ll do a recap of the key stages of building wealth. A sort of end of topic summary if you will. Something to show how crazily straightforward building wealth can be…

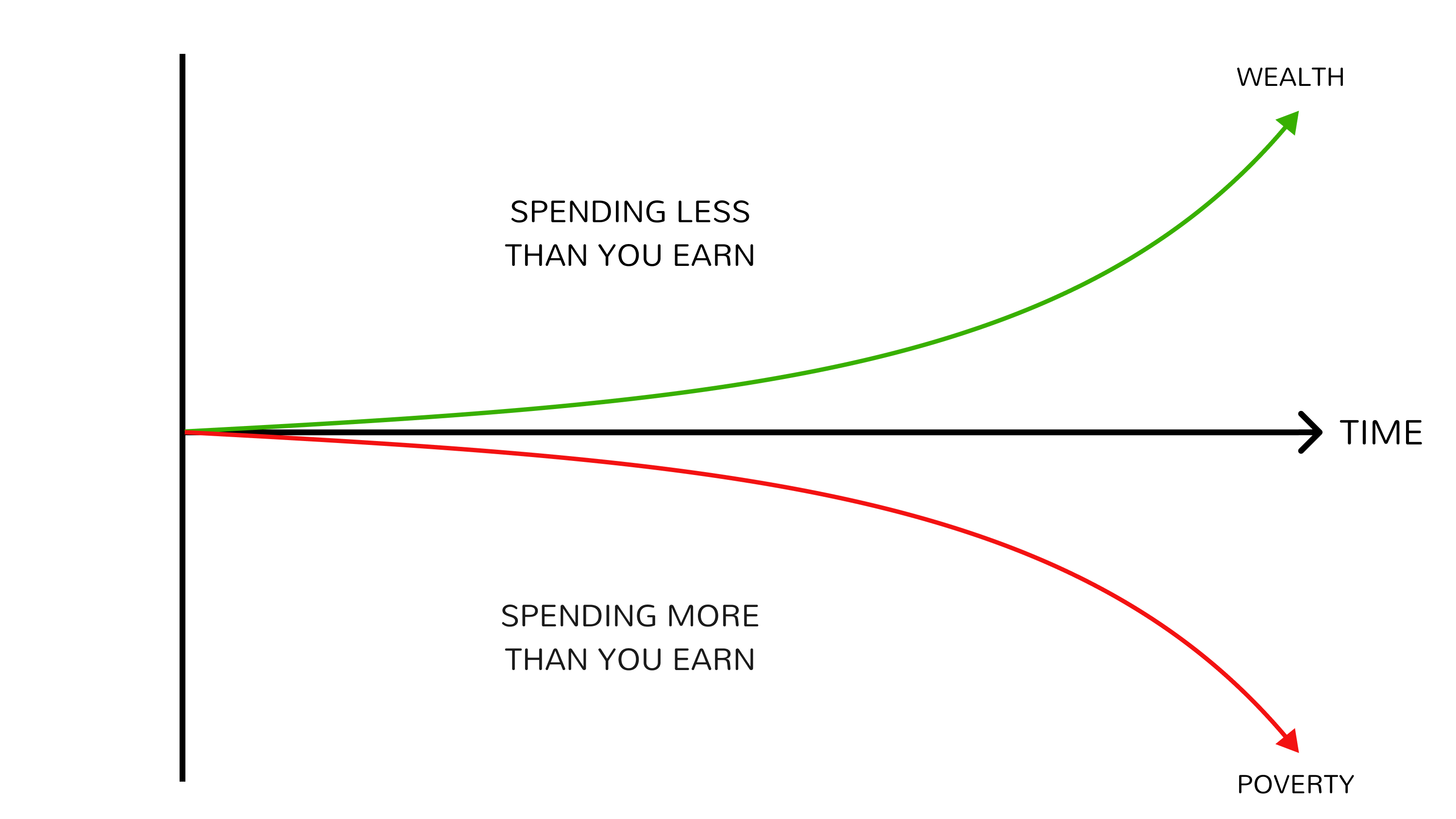

Reduce Excess Spending

The key word here is “excess”. It doesn’t matter what you earn, if you spend the same or more, you’ll never build long term wealth.

Your whole ability to save, invest and improve your personal finances depends on your ability to manage your money and resist spending all of it.

As we progress and develop in our careers, we tend to earn more and more money, with the natural response being to spend that money on buying ourselves slightly nicer things. Eating out more often, going to more expensive shops, driving more expensive cars etc.

This lifestyle creep makes us feel important, that we’re becoming someone.

What it’s actually doing is adding on years to the point where you’re financially free. Your boss loves it when you turn up to work with your new watch and car, because he knows that he just locked you in for a few more years.

Keep hold of your money. It’s your key to freedom.

Build an Emergency Fund

The all important emergency fund (see more here). One of the most crucial parts of building wealth.

You need to have a savings account with money that you can easily access. Start out getting it to £1-2k, and then once your high interest debts are paid down, build it up to 3-6 months of expenses as a minimum.

At the beginning, this is to protect you. Imagine that you have no savings (as is the case with about 34% of Britons) and your car breaks down. If you don’t have the money to pay for the repairs, there’s a very real risk that you have to take on debt to pay for the repairs.

Having the money there allows you to pay for these curveballs, these unforeseen circumstances and situations that life throws your way. Sure, they’re still unwelcome, but at least with some money set aside, they won’t ruin you financially.

Once you have paid down your high interest debts (which we’ll cover in the next point) your emergency fund is all about building what can be known as a “Freedom Fund” or, depending on your preference, “F*ck You Money”.

This is money that you can use to start a business, to take a chance on a career change. If you’re made redundant suddenly, that money will cover you until you can get back into another job.

It’s your own insurance, only without the hassle when you need to make a claim.

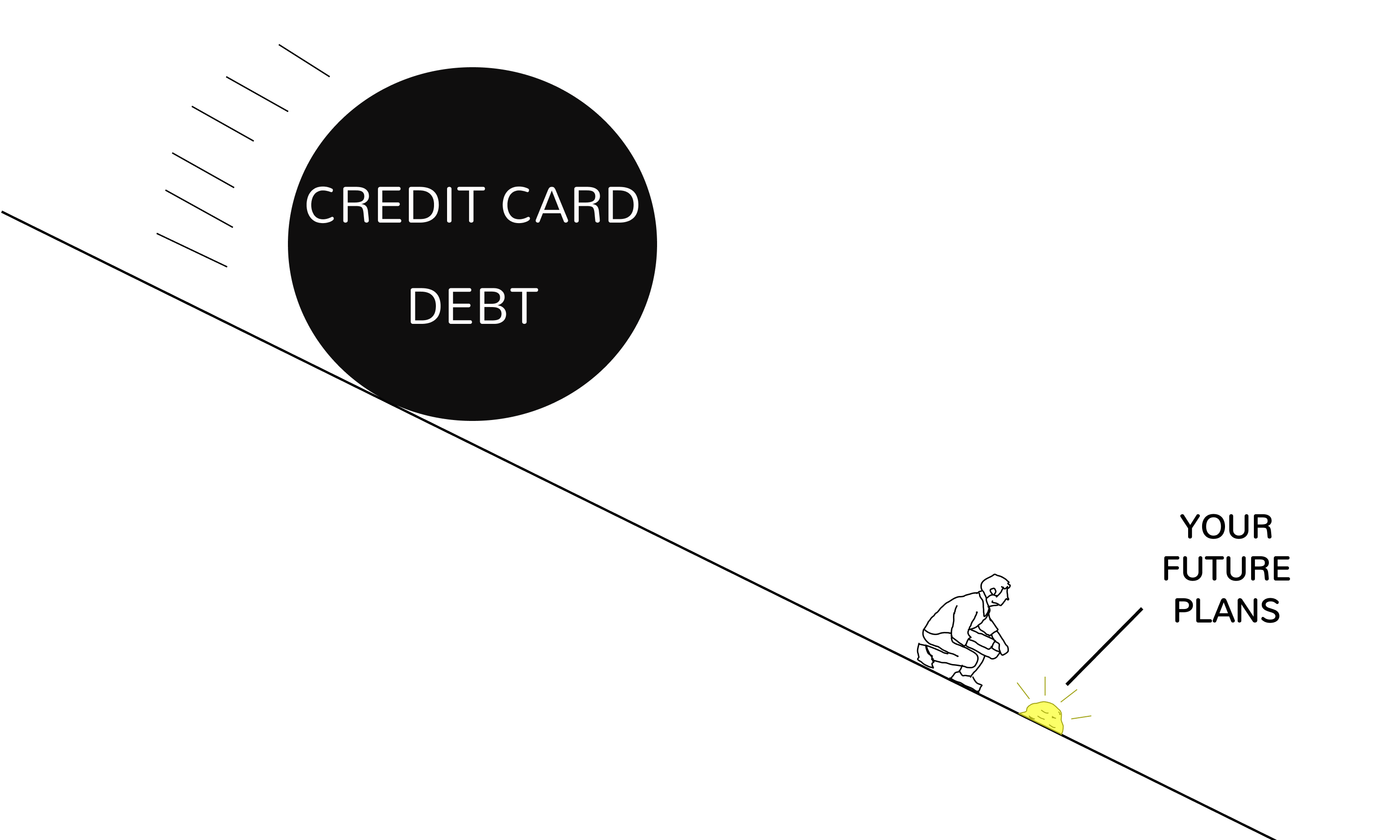

Pay off High-Interest Debt

After you build your initial emergency fund, and before you save up your 6 months of expenses, you need to focus on paying off your high interest debt.

Credit cards often have interest in the region of 20%. This means that if you don’t tackle them soon, the debt can build up very quickly (see here).

By focusing on paying off these debts (not just the minimum payment, but as much as possible) you reduce the amount of interest added by the lender.

If your debts (against you) are increasing by 20% and your savings account (for you) is growing by maybe 1-2%, it comes down to simple maths. The increases in debt will wipe out any increases in growth from savings.

Get rid of that shit, and fast.

Increase Earning Capacity

The problem that many people have when it comes to trying to build wealth is that they think it’s a matter of saving more of what you earn.

The problem is, you will always have expenses. And moving into your old bedroom, eating noodles every day and walking everywhere in second hand clothes isn’t much fun for most of us.

If you try to reduce your expenses, that’s great if you want to save your money, but you will always be limited by what you earn. There is a ceiling.

On the other hand, if you focus on increasing your income, there is potentially limitless upside. By changing jobs or getting a pay rise, you might now be earning £10k a year more. Add a side hustle onto that and you could be looking at another £5k a year.

Decreasing your unnecessary expenses is good. But focus on the unlimited potential of increasing your earnings (see here) and you can save more without having to become the most frugal (cheap) person you know.

Invest in Assets

Finally, once you have all of the above under control, it’s time to focus on investing.

You don’t need to be wealthy to start investing, but you do need to invest if you want to be wealthy.

You simply cannot save your way to wealth. For a start, inflation will always eat away at the value of your money, making it worth less and less every year.

This is an unavoidable step, and the good news is that it doesn’t have to be complicated.

You can invest in real estate to rent out, or you can invest in cryptocurrencies, which depending on your approach, is either a no-brainer, or roughly the same as playing roulette.

The easiest, most straightforward way is to regularly invest into an Index Fund. These funds simply track a certain Index and by investing in the fund, your money is divided over all the companies in said fund. Your £100 buys you a bit of Apple, some Microsoft, a side of Tesla and some Google to boot.

Set it to automatic, and as your earnings increase, ramp up the contributions. Reinvest the dividends back into the fund, and watch as your net worth slowly but surely moves upwards and to the right.

Now go and buy yourself a bottle of (reasonably priced) champagne.

You’re well on the way to financial independence.

I’ll cheers to that!